Investments 101: High Yield Corporate Credit: Don’t Worry, Be Happy?

The US high yield corporate bond market is pricing in benign news for future credit defaults. How credible is this message? How might this impact other parts of your investments?

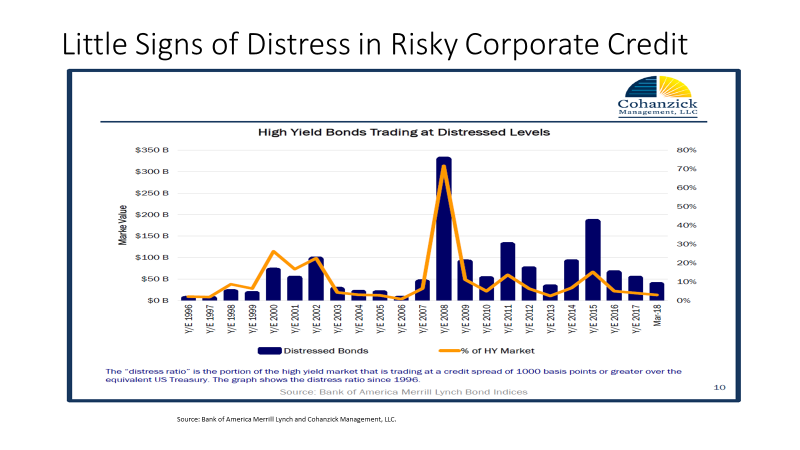

The above chart suggests high yield corporate bonds are enjoying calm weather.

Data compiled by Cohanzick Management, a New York-based asset manager, and Bank America show the amount of US high yield corporate bonds[1] priced as if they were going to default in the near future. The data include corporate bonds that trade 10% or more (1,000 basis points) above the yield of the equivalent US Treasury bond. Such bonds appear to sport high yields, but they do so with a reason: fear that the company could choose not to pay bondholders back and default. Think Toys R Us as one recent example of a company that eventually went bankrupt.

The blue bars represent the absolute level (market value) of bonds priced for bankruptcy for a given year.

The yellow line shows the percentage of the total high yield market that is priced as if it were going to default.

Whether an issuer priced as distressed actually defaults or not depends on the situation. Often the market is correct about such dire prospects. Sometimes, the market overly panics, and the company manages to find a way to bail itself out. What matters for this discussion, though, is this: what message is the high yield market sending about the US economy overall?

Currently, the level of bonds priced for default is about 3% of the total US high yield market. This is close to the lows set earlier this century. While this number appears good for the moment, there are also reasons to be concerned.

Defaults at this level are likely to get worse, not better, based on past history. Two historical precedents for a bear case going forward might include:

- 1999: TMT[2] on the eve of the dot-com bubble bursting, when the Fed also had just been hiking interest rates aggressively after pumping in excess liquidity to stave off contagion from the Russia debt default/emerging market crisis to the US. High yield defaults were concentrated mainly in those sectors, but the economy later turned into recession, and stocks corrected.

- 2006: The housing bubble was about to burst. The Fed was raising interest rates while oil was over $100 a barrel. It took another 2 years before we finally entered the Great Recession. Numerous sectors experienced high defaults. Stocks corrected.

A more benign case might consist of something like 2003. Interest rates remained quite accommodative for a long time. Steady economic growth and reasonable interest rates prolonged a benign credit cycle for years. Eventually, however, it gave way to asset bubbles particularly in the housing and debt markets.

What lessons might we learn for today?

Economic recovery, while the second longest on record, has also been tepid, as evidenced by the weakest level of growth in recorded US history. The hangover from the financial crisis has allowed central banks to keep interest rates low even after recent rises. Additionally, low inflation has also resulted in robust profit margins for many companies.

However, any change in inflation might make central banks tighten short-term interest rates more aggressively. Cost pressures from either wage or input price inflation might weaken corporate margins. A combination of these two issues might put pressure on certain issuers in the high yield market. That might send a warning signal to corporate credit and adversely impact other assets, including equities.

[1] “A high-yield bond is a high paying bond with a lower credit rating than investment-grade corporate bonds, Treasury bonds, and municipal bonds. Because of the higher risk of default, these bonds pay a higher yield than investment grade bonds. Issuers of high-yield debt tend to be startup companies or capital-intensive firms with high debt ratios.” Source: Investopedia, https://www.investopedia.com/terms/h/high_yield_bond.asp accessed on May 17, 2018.

[2] “What is the ‘Technology, Media, and Telecom (TMT) Sector” on https://www.investopedia.com/terms/t/technology-media-and-communications-tmc-sector.asp accessed on May 17, 2018.