How Bad Trades in Volatility Have Exaggerated the Recent Sell-off

- The market has entered a true correction

- Reasons not to panic, but technical factors might take time to clear out

- We remain cautiously optimistic in absence of major change in fundamentals

As of market close on February 8, 2018, the S&P 500 has corrected more than any time in the last year.

Some of the reasons are fundamental (high valuations in most asset classes), but the extent of the recent sell-off appears more technically driven.

The drawdown in the S&P 500 from peak to trough prices in 2018 is approaching -10%, which already far exceeds the very modest drawdown of -3% in all of 2017 and breaks the streak of over a year without a -5% correction. On the flip side, this recent correction is below the -20% drawdown in 2011 (when fears of Greece bringing down the Euro weighed on markets).

What is really upsetting the markets this week? The bomb that some investors did not understand.

This is not a story of Exchange Traded Funds failing the market. This is partially a story of certain investors speculating on the world becoming a calmer place (and getting it wrong).

Chart Showing Exchange Traded Note that Bets on Falling Volatility

Exchange Traded Products (ETP’s) have made it easier for retail investors to access alternative asset classes once limited to large institutional investors. One such alternative asset classes is “volatility”.

Simplistically, “volatility” is taking a view on the turbulence (or calm) that major market indices should experience in the future. Investors taking a constructive view of rising volatility anticipate a wider range of market changes, even if they do not know whether the change is positive or negative. In other words, a positive view on volatility implies more response (fear or greed) in regards to the future. (Though, as we have seen recently, higher volatility tends to occur more frequently with sharper market declines than advances.)

Conversely, investors taking a negative view on volatility believe markets are overreacting to future events in either direction (or a view of “Don’t worry, be happy”). Such investors could ground their caution on volatility due to the fact that central banks will intervene in either direction if markets get too out of hand.

ETP’s exist both for bulls and bears on “volatility”. Until recently, investors betting against volatility have made a killing on such investments. That is, until February 2018.

Chart Showing Exchange Traded Note that Bets on Rising Volatility

Insurance companies and certain institutional investors trade volatility to hedge their books. That would appear to be the contributor to the recent roller-coaster ride in markets. (The huge spike in the blue line in the bottom chart above might reflect these technical factors, which in past years have ultimately dissipated.)

The magnitude of the correction is not outsized relative to corrections within bull markets. The speed that it took place absent from major fundamental news suggests technical factors, like perhaps an unwind in negative volatility trades, are exacerbating it.

If this proves to be the case, there is potential for the market to stabilize absent adverse changes in fundamentals. We remain cautiously optimistic.

(Full disclosure: Ambassador clients did not and do not have exposure to the ETP’s discussed in this blog.)

Chart Showing Exchange Traded Note that Bets on Rising Volatility

Some things to put into perspective:

- US economy near-term shows no signs of recession.

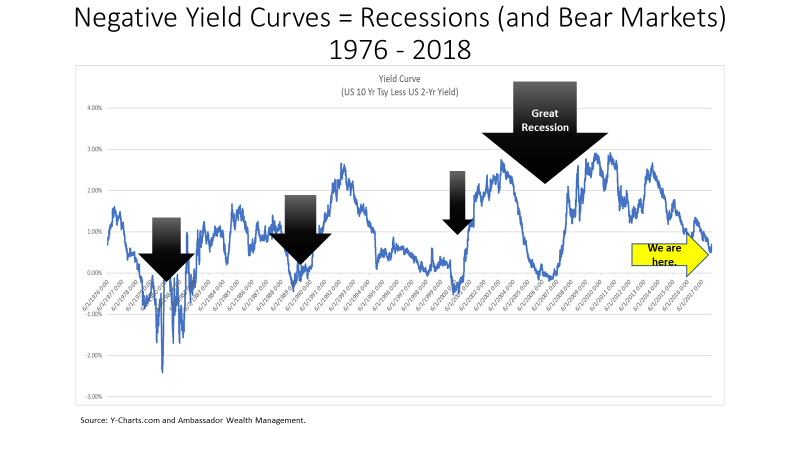

- Yield curve is positive (though much less so than recent past).

- Generally, when longer-term interest rates are greater than shorter-term interest rates, the US economy is expanding.

- When shorter-term interest rates exceed longer-term rates, that has signaled a deterioration in US economic activity. (See the black arrows that show economic recessions.)

- Markets correct in the face of economic recessions (and declines in corporate profits).

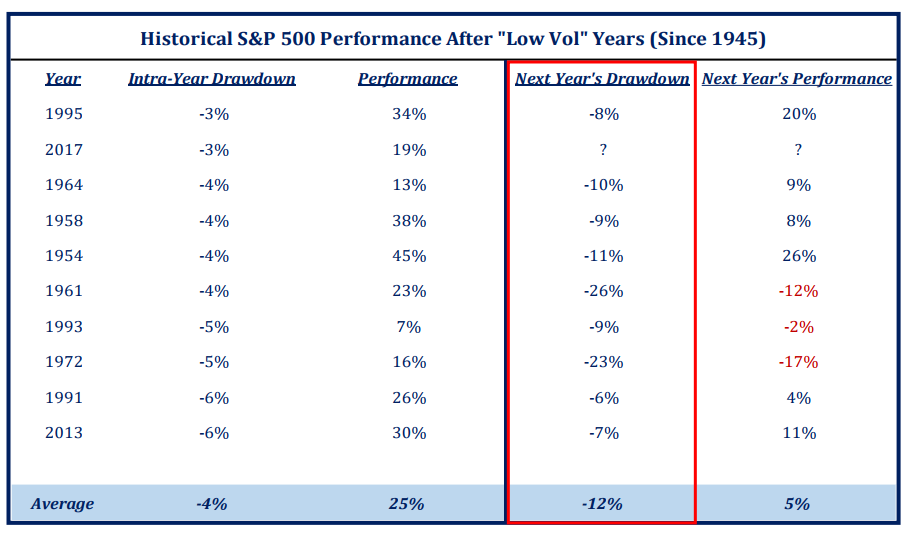

- We were due for some selling following an unprecedented run in the market over the last year. As research house Strategas cites, strong years with low volatility might often presage higher volatility in the following year. Drawdowns (defined as declines from market peak to trough) of -6% or more are common. However, 6 of 9 such years still resulted in market gains for the year, albeit less dramatic than the year before.

Source: Strategas - Good economic news is a mixed bag for the markets.

For example, the January jobs report showed decent jobs growth, lower unemployment, and an uptick in wages. Market players got spooked that the Federal Reserve would hike rates further and risk slowing the economy too much.Recent strong market gains in January also have left valuations high, even though the strong economy generally has resulted in a positive 4q earnings report season.

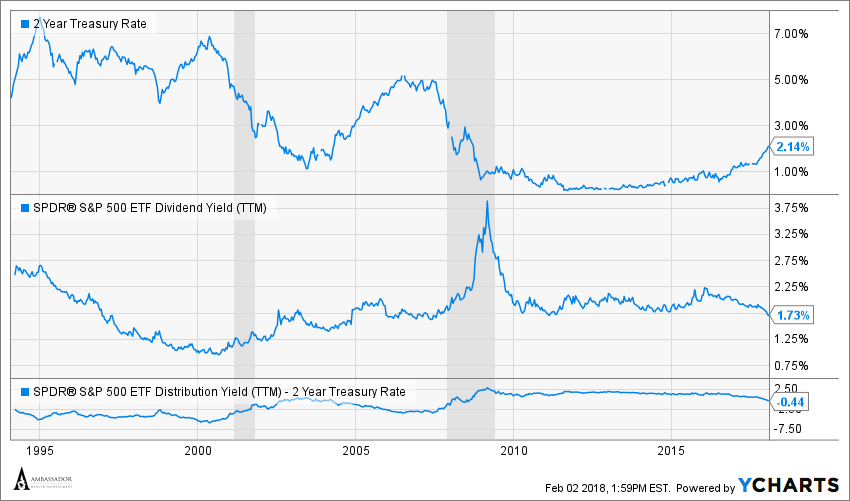

Recent history over the last 25 years suggests that while future market gains might slow, the level of interest rates themselves might not derail the market in and of themselves. The chart below shows that the yield on 2-Year Treasury Bills now exceeds the dividend yield on the S&P 500 for the first time in nearly a decade (post-2008, the Great Recession or Global Financial Crisis).

However, taken over a longer timeframe, 2-Year Treasury yields have actually been much higher both in absolute terms and even relative to the dividend yield of the S&P 500. Given what we know about the current environment, a further rise in the 2-Year Treasury from current levels of 2.1% to say 3.0% might not necessarily pressure that of the S&P (at least based on history from the economic expansions earlier in the mid-2000’s and mid-1990’s).

The one signal we would be wary of is signs of economic recession (gray shaded areas in the graphs). If history were to repeat, that might portend a market correction of greater magnitude. For reasons that will be discussed in a future blog, we believe a recession is unlikely in the near term.

Source: Ycharts.com and Ambassador Wealth. - We remain cautiously optimistic on select risk assets in 2018. As we discussed in our 2018 Investment Outlook, economic fundamentals are constructive (not only in the US), but valuation is full to excessive in many areas.

Some market pundits are more bullish:

“A market surge is ahead. If you’re holding cash, you’re going to feel pretty stupid.” Ray Dalio[1]

“I recognize that we are currently showing signs of entering the melt-up phase of the bull market.” Jeremy Grantham[2]

“The game of economic miracles is in its early innings. The world is getting better.” Warren Buffett[3]

What we like:

- Cautiously optimistic on equities (still cheaper than fixed income)

- Broader exposure beyond S&P (Japan, small cap, small portion of emerging markets)

- Liquid absolute return strategies less correlated to equities or fixed income (call writing)

What we dislike:

- Much of fixed income (duration, most credit expensive)

- Europe

- Many illiquid “alternative” strategies

[1] https://www.cnbc.com/2018/01/23/ray-dalio-says-market-surge-may-be-ahead-if-youre-holding-cash-youre-going-to-feel-pretty-stupid.html accessed on February 2, 2018.

[2] https://www.bloomberg.com/news/articles/2018-01-03/gmo-s-grantham-says-stocks-could-be-heading-for-a-melt-up accessed on February 2, 2018.

[3] https://www.bloomberg.com/news/articles/2018-01-04/warren-buffett-remains-optimistic-about-america-s-future accessed on February 2, 2018.