Investment Newsletter 2Q19

An Update on Our View of the World

After one of the worst quarters in a couple of years, risk assets recovered strongly in 1q19. Stocks, commodities, and bonds, for the most part, posted positive gains. Possible reasons include:

- Continued strong corporate profits especially in the US

- Economic growth in US still positive though weaker (less so internationally)

- Declining bond yields

- Stabilization in oil prices owing to OPEC agreement to cut oil production

- Hope for China growth to turn around, including a potential truce in the trade war

| Start Date | 9/20/2018 | 12/30/2017 | 12/31/2018 | ||

| End Date | 12/31/2018 | 12/31/2018 | 3/28/2019 | ||

| Ticker | Name | Correction | CY 2018 | YTD 2019 | |

| IVV | iShares Core S&P 500 ETF | -14.1% | -4.6% | +12.5% | |

| IWM | iShares Russell 2000 ETF | -21.3% | -11.1% | +13.6% | |

| ACWX | iShares MSCI ACWI ex US ETF | -12.0% | -13.9% | +9.3% | |

| EFA | iShares MSCI EAFE ETF | -13.4% | -13.8% | +9.7% | |

| IEMG | iShares Core MSCI Emerging Markets ETF | -7.6% | -14.9% | +8.2% | |

| AGG | iShares Core US Aggregate Bond ETF | 2.0% | 0.1% | +2.9% | |

So, are the good times back for good? We think a healthy dose of skepticism might still be appropriate.

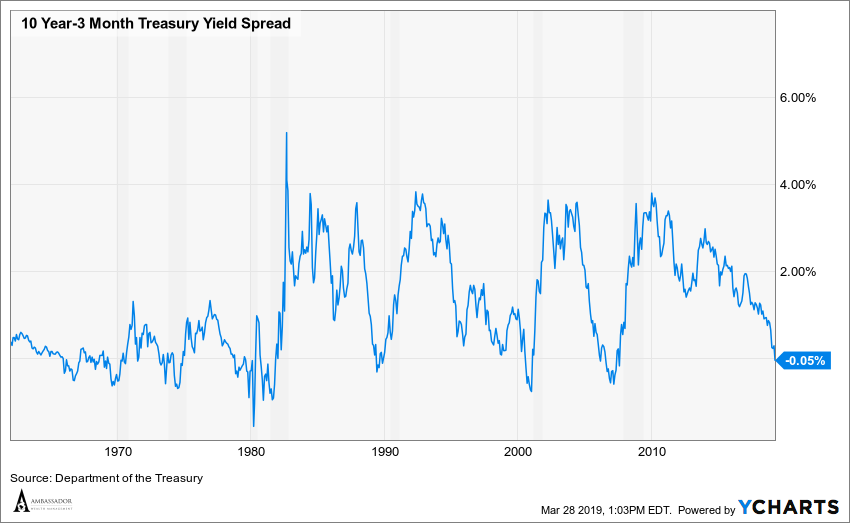

We have previously commented on the slope of the yield curve as an indicator of economic health. When the line is moving up, historically that has often signaled economic expansion. When the line moves down, one needs to be more cautious. “But when the yield curve turns negative, all bets are off.”

Today, the difference between long term bond yields (10-year US Treasury) and short-term interest rates (3 Month T-Bills) is a -0.05%. That might augur a cautious outlook for the economy and risk assets.

One potential mitigating factor is that comparable international bond yields are even lower. For example, current 10-year yields in the US of 2.6% exceed yields of 0-1% in Japan, UK, and Germany for similar bonds. Apparently, global bond managers might be to blame rather than a necessary weakening in US economic fundamentals. Perhaps US bonds might be priced higher (and the slope more positive) were it not for low international bond yields?

Our read is somewhere in the middle between bull and bear. While jobs and consumption continue to grow (mainly in the US, to a lesser degree in emerging markets), other areas of the global economy are stalling or even declining. Corporate earnings growth is clearly decelerating.

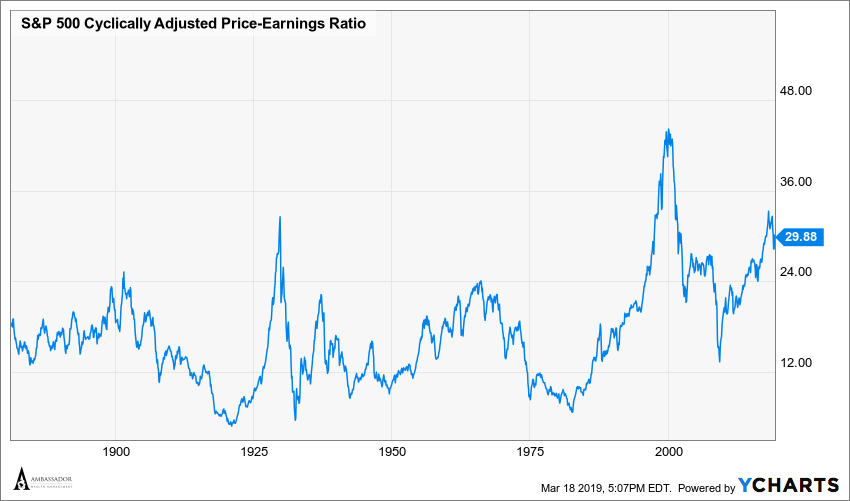

When you factor in that markets now are also back toward the higher end of history (off both recent troughs and bubble peaks), we have a neutral tilt toward risk in portfolios.

How Are Your Portfolios Being Positioned?

Your portfolios are constructed based on 3 buckets. Depending on your specific financial situation, you might have a greater weighting in a bucket versus the others. Included are some brief updates:

- Income – goal is to clip coupons with low to moderate variation in price

Update: we added an active total return manager with expertise in consumer and muni bonds. This might enhance yield with a modest increase in credit risk.

- Growth – goal is strong capital appreciation with high potential price variation

Update: we added exposure to an emerging market consumer goods ETF that might benefit from growth in the middle class in emerging markets. We also took profits on US small cap, REIT’s, and Japan.

- Diversification – goal is moderate capital appreciation with moderate variation in price; some elements reflect hedging against macro events

Update: we added 2 new strategies to your portfolio: merger arbitrage and equity long/short. Both strategies potentially offer positive returns with moderate exposure to traditional equity and fixed income risk. The manager of the strategy had run another larger successful fund at another firm.

Please let us know of any questions. You can also find a lot of information on a variety of investment topics on our website.

Sincerely,

Stuart P. Quint, CFA

Managing Director, Investments and Compliance