Investment Newsletter 3Q19

Investment Newsletter 3rd Quarter 2019

“Dull” quarter? Not really…

Dear Ambassador Family,

We have not changed much since the last letter – 3 on a scale of 1 to 5. The strong rally in 1q19 is flattening out as corporate fundamentals are modest but solid. Low interest rates thus far have limited downside.

Since the last newsletter, we have moved slightly more negative on the US Dollar. This continues a trend from last year of adding gold and emerging markets (depending upon your family’s model and risk tolerance). Slower growth, a potential cut in interest rates, and volatility from upcoming elections next year are the main reasons.

Over the last several months, we have been reviewing client portfolios and taking down risk to specific factors (trade war, exposure to negative yield curve, most cyclical commodities).

Gold and Treasury bonds have rallied in 2q19 as investors sense a more dovish Fed. S&P 500 is holding onto a slight gain with solid corporate fundamentals continuing to be offset with high valuations. Small cap and international markets are slightly down for the quarter.

Do not let the lack of big price moves fool you. Cross-currents in the global economy remain:

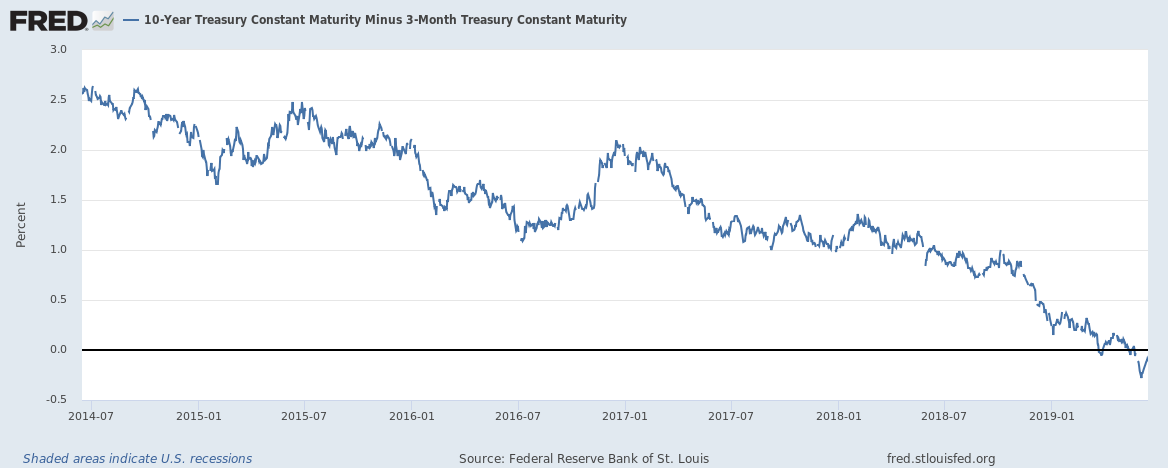

- The US yield curve remains inverted – though, now, Fed has tipped its hand that it might lean a little dovish (e.g. likely to cut rates now rather than raise them).

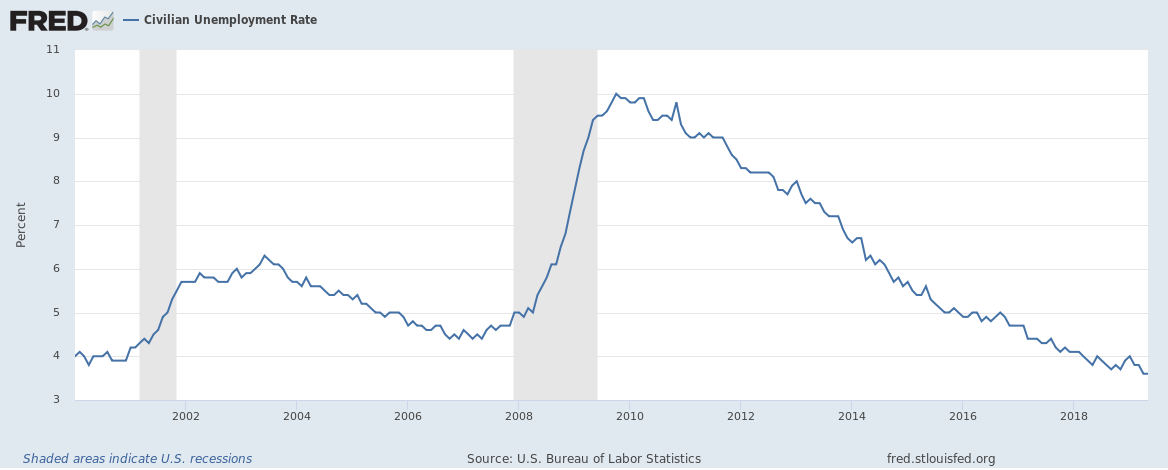

- US economic growth has been steady but unexciting. Jobs gains are positive but well off the peaks. Inflation is subdued.

- International growth continues to be weak in general.

- The US and China are now unlikely to come to a trade deal in the near term. Markets have been surprisingly resilient.

- Geopolitical tensions with Iran might be rearing their ugly head (though that has not boosted oil much)

- Markets have generally yawned about European elections (more populists in power, but not enough to get excited) and risk of a disorderly Brexit.

- It is early, but US presidential elections in 2020 might add some market volatility.

We continue to be hopeful for gradual gains. Yet, we are also mindful that risks at current high valuations remain.

Please let us know of any questions.

Sincerely,

Stuart P. Quint, CFA

Managing Director / Investments and Compliance